Business Insurance

Full article on businessinsurance.com

Author: Louise Esola

Long-term health issues following a COVID-19 diagnosis will likely affect workers compensation claims acceptance, management and disability indefinitely, experts say.

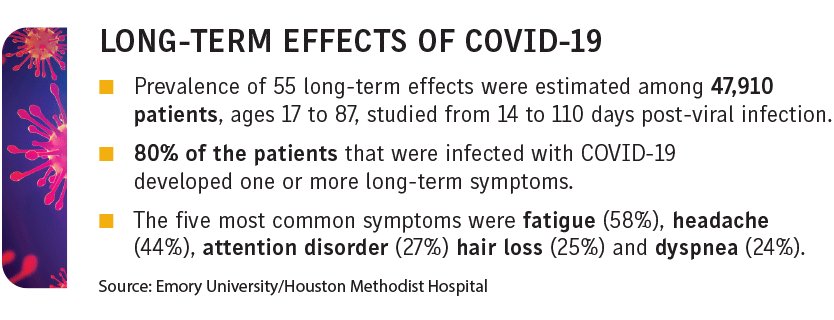

Under the catch-all phrase “long COVID,” symptoms include fatigue, chest pain, shortness of breath, joint or muscle pain, and difficulty concentrating. At least one study (see box) found 55 possible long-term effects of COVID-19.

“Navigating a patient through long COVID or long-hauler syndrome really is uncharted territory,” said Kathy Galia, senior vice president and general manager of clinical solutions for Paradigm, which provides managed care for injured workers, during a webinar in July.

While no official number is available, some organizations estimate that up to 80% of COVID-19 patients will experience one or more long-term, persistent symptoms.

“We’re in the long haul,” said Beth Burry-Jackson, Richmond, Virginia-based senior vice president of case management for Sedgwick Claims Management Services Inc., of the complicated scenario of managing COVID-19 claims with long-term symptoms.

Symptoms are diverse, require care from different kinds of practitioners and much coordination is needed among providers, she said.

“A vast number of medications have been thrown at the symptoms,” Ms. Burry-Jackson said. “There is no protocol, because the symptoms are so vast (and) these are imprecise symptoms, not where you can prescribe something and be done. What we are looking at is developing some best practices along the way.”

Data is limited on the costs associated with long-term COVID-19 care in the comp system, said Jeff Eddinger, senior division executive for the Boca Raton, Florida-based National Council on Compensation Insurance, which has been tracking COVID-19 claims costs since the start of the pandemic.

Most claims, he said, are indemnity only, which don’t include medical costs and only support income while an affected worker is out recovering from the virus.

According to the latest figures from NCCI, workers hurt by COVID-19 accounted for more than 45,000 claims in 2020, with more than 95% costing less than $10,000. Most of the claims closed quickly, and only about 1% surpassed $100,000, Mr. Eddinger said.

“I’m not suggesting that we shouldn’t keep an eye on long-term COVID claims,” he said, adding that “the system is healthy in handling the COVID claims. It has not put a strain on the workers compensation industry” thus far.

Those managing cases should be wary that might change, however, especially as long COVID now falls under the guidance of disability management, experts say.

“We are just beginning to understand the long-term damage that the disease is causing for a significant portion of patients,” wrote Phil Walls, Tampa, Florida-based chief clinical officer for myMatrixx, an Express Scripts company, in an email.

Mr. Walls said that “accepting compensability for a COVID claim may incur costs well beyond the potential hospitalization and initial phase of treatment.”

“For those patients that develop more severe post-COVID symptoms … the treatment and its costs may continue for the life of the patient. Other symptoms may not incur the same treatment costs but will create other concerns, including disability,” he said.

The Office for Civil Rights of the Department of Health and Human Services and the Civil Rights Division of the Department of Justice in July provided joint guidance on long COVID, which is now considered a disability — a threshold that typically comes with implications for the comp industry.

Diana Tsudik, an Anaheim, California-based partner with the Employer Defense Group LLP, said that employers are beginning to see long-hauler COVID-19 workers comp claims from individuals who never filed an initial comp claim at the time of infection, complicating the acceptance and investigation processes for claims handling.

“There’s no correlation between the initial symptomology” and long COVID, she said.

“If somebody didn’t file that (initial) claim, it is a lot harder for me to get information on the initial infection and how that came about. It puts insurance companies and employers behind the eight-ball. What do you do with all those claims that were not in the outbreak but now are in the outbreak? For a lack of better terms, it’s a mess.”