Business Insurance

Full article on businessinsurance.com

By: Danielle Ling

COVID-19 infection claims proved to be relatively inexpensive last year for the workers compensation industry, which entered 2022 on a stable basis, industry experts say.

The market managed to withstand a previously negative outlook in 2021, which A.M. Best & Co. later revised to “stable” due to the surprise “muting” effect the COVID-19 pandemic had on insurers’ operating performance and balance sheets, solid risk-adjusted capitalization, redundant loss position and favorable combined ratios.

Additionally, strong retention rates were widely reported by workers compensation insurers in 2021, many of which exceeded pre-pandemic levels, according to Dan Mangano, Bridgewater, New Jersey-based senior financial analyst at Best.

However, that may be due to agents or brokers being reluctant to move accounts, Mr. Mangano said, highlighting the intensifying competition in the market.

“Despite its general stability as a line of business, there’s definitely some volatility in the environment right now, particularly with some key variables that directly impact workers comp like interest rates, inflation, the economy and the recovery, unemployment and uncertainty with COVID,” said Coleman Johnson, Boston-based chief underwriting officer for the U.S. middle market at Liberty Mutual Insurance Co.

“I don’t think it’s as easy to peg exactly where those trends are headed and what that means for pricing in the market as it might have been in the past,” he said.

Inflation is a top concern for many industry executives.

In a presentation identifying workers compensation trends, Kimberly George, Chicago-based global head of innovation and product development at Sedgwick Claims Management Services Ltd., echoed a common narrative across the industry, calling 2022 “the year of fighting inflation.”

This year will see the strongest rate in 39 years, with prices rising in the first half “due in part to the ongoing supply chain concerns and the lack of workers,” Ms. George said.

“If inflation doesn’t fall as rapidly as hoped, the Federal Reserve may raise rates more aggressively, which leads to the concern of market stability,” she added.

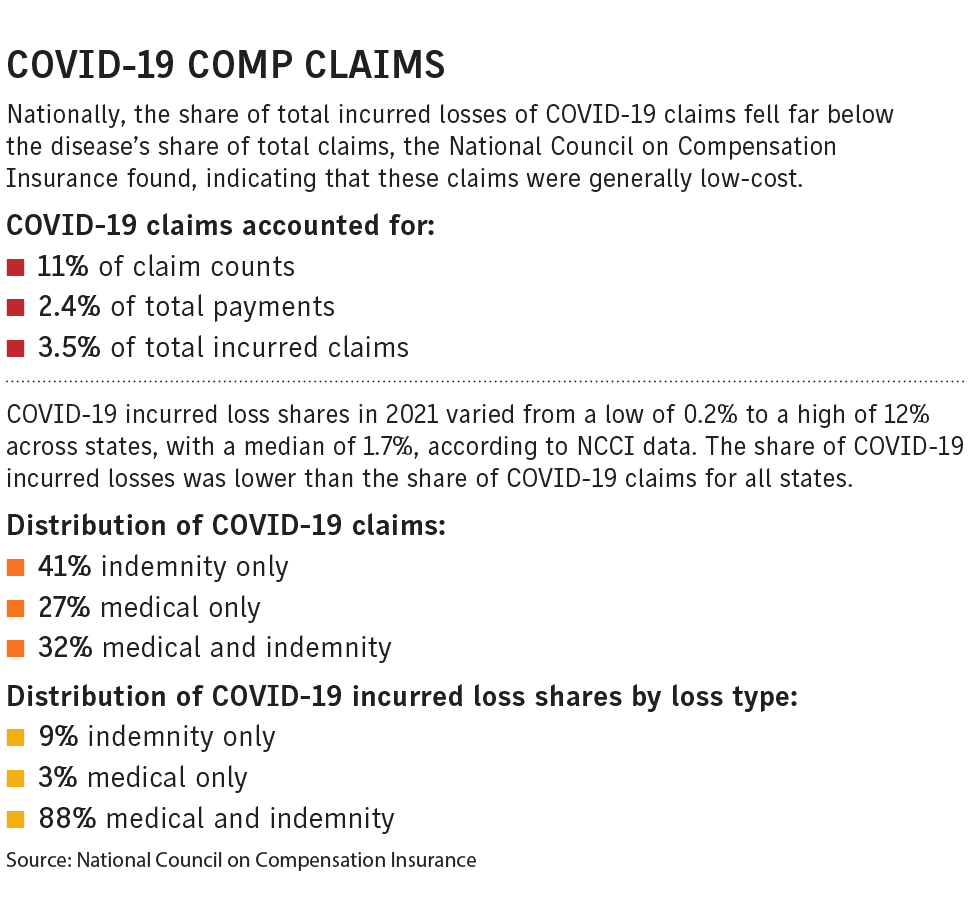

An issue identified by industry executives in a survey by the National Council on Compensation Insurance is rising medical costs, according to Jeff Eddinger, NCCI’s Boca Raton, Florida-based executive director and actuary.

“The fact that we’re seeing inflation in a lot of areas means that we could also be seeing general medical inflation, which has been pretty low in recent years,” he said, adding that “if that were to spike up, that could be a cost driver to make some claims more expensive.”

The widespread labor shortage could also affect comp financials this year, said Debbie Goldstine, Chicago-based executive vice president of U.S. casualty, technical intelligence and emerging risk at Lockton Cos. Inc.

“The labor shortage impacts workers compensation in many ways,” said Mark Walls, Chicago-based vice president of client engagement at Safety National Casualty Corp. “First, premiums are tied to payrolls, so less workers means less premiums.”

Despite some offset by higher wages, industry premiums are down in almost every state, he said.

Labor shortages also lead to increased hiring of “new, less-skilled workers,” which historically means increases in claims frequency in workers comp, Mr. Walls said.

“Add that to an already positive severity for the line for medical and indemnity, and the frequency of large losses continuing to climb, there’s an increasing loss cost that we have to keep up with if we want to have a stable, healthy comp market going forward,” he said.

Effect of long-haul COVID on comp claims remains unclear

The COVID-19 pandemic will continue to dominate the workers compensation narrative in 2022, but the conversation may shift to concerns over advancing occupational illness legislation and the mysteries surrounding long-haul COVID.

Long-haul COVID has so far had little effect on workers compensation, but that’s because the understanding of it is so new, “dynamic” and “confusing,” said Dr. Michael Choo, Wilmington, Ohio-based chief medical officer and senior vice president at Paradigm Corp.

In a recent report, Dr. Choo presented the challenges of long COVID in both understanding the disease and measuring its effect in patient numbers, costs and claims. A recent study found patients reported an average of 21 symptoms, he said.

The U.S. Department of Health & Human Services and the U.S. Department of Justice in July 2021 recognized long-haul COVID, as it is sometimes called, as a federally classified disability, providing protection under the Americans with Disabilities Act to workers suffering from it.

Dr. Choo noted that few patients have been diagnosed with long COVID.

“Since the actual number of people with long COVID is unknown, a critical question remains the size and scope of this issue with respect to potential impacts to our workforce, employers and the workers compensation industry,” he said.

Meanwhile, as workplace issues related to COVID-19 infections and vaccinations evolve, states are likely to continue to consider further COVID-19 and infectious disease workers compensation presumption legislation this year.

At least a dozen states in 2021 introduced legislation to establish presumptions for infectious diseases and pandemics, according to NCCI. Tennessee and Washington enacted legislation.

“There’s no question that this isn’t an issue that’s going to just dramatically go away,” said Mark Walls, Chicago-based vice president of client engagement at Safety National Casualty Corp. “This is a new frontier for workers compensation and one that is really tough from a risk management standpoint to deal with.”